Area A: Foundations

Individual Behavior under Uncertainty in Dynamic Environments

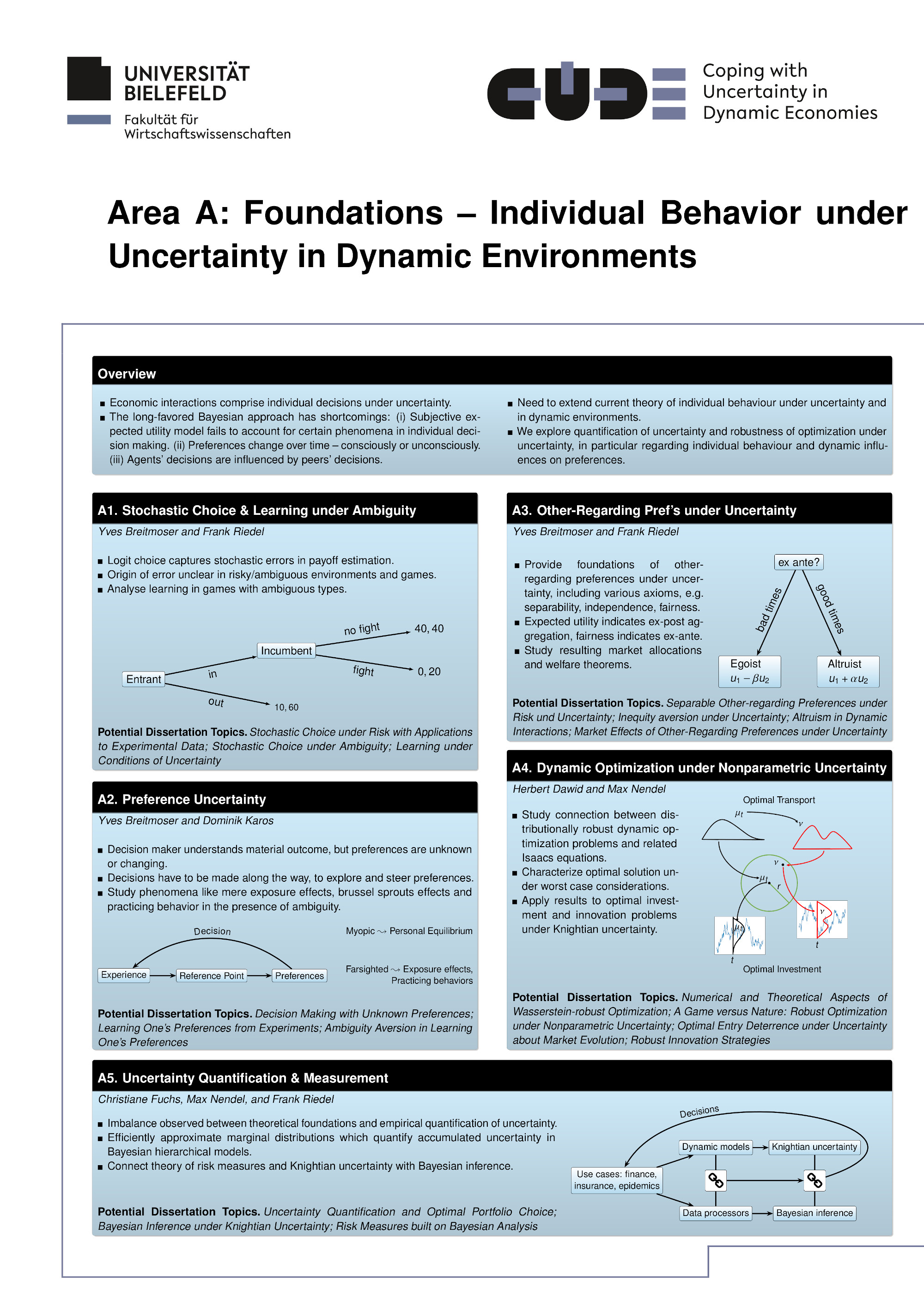

At its core, any economic interaction comprises one or several individual decisions. Each decision involves evaluations of outcomes, of beliefs, and of the dynamic evolution of relevant economic factors, all of which may be uncertain from the perspective of the agents. Economists have long favored a Bayesian approach towards the resolution of these uncertainties, as justified axiomatically by Savage and Anscombe-Aumann. This approach has several shortcomings, however. First, both conceptionally (Ellsberg, 1961; Gilboa and Schmeidler, 1989) and empirically (Camerer, 2003), the subjective expected utility model fails to account for many phenomena surrounding individual decisions. Second, even if the probabilities of events could be learned by experience over time and, thus, allow for a Bayesian approach, preferences themselves tend to change over time. This can happen unconsciously (see for instance the “mere exposure effect”, Zajonc, 1968) or consciously, as decision makers can influence their preferences on purpose and “acquire a taste” over time. Third, in a social context, it is by now well documented (Bolton and Ockenfels, 2000; Breitmoser and Tan, 2013; E. Fehr and Schmidt, 1999) that agents’ decisions are influenced by their peers’ decisions and well-being. In many interactions, it is therefore important to account for other-regarding preferences as well. Similarly, economic agents tend to make at least stochastic mistakes, but there is more than one way to think about stochastic choice under uncertainty—which way should we use?

As these points illustrate, once we attempt to take the notion of (persistent) uncertainty seriously, we will quickly find it necessary to extend the current theory of individual behavior under uncertainty and specifically in dynamic environments. Applied work further benefits from the development of new ways for the quantification of uncertainty and from the assessment of the robustness of optimization methods with respect to uncertainty. These are the main objectives of Research Area A of this proposal.

Specifically, we intend to explore individual and social decisions under uncertainty from new perspectives. In overall five projects we shall investigate the prospects of ambiguous or stochastic choice and of learning under uncertainty (A1); we shall search for optimal dynamic decision making of individuals who learn or influence their preferences over time (A2); we shall combine other-regarding preferences with ambiguity in competitive market models (A3); we shall extend the theoretical foundations for robustness analyses of optimal dynamic investment strategies (A4); and we shall advance the quantification of uncertainty and research the resulting optimization problems for individuals (A5).