Statistical modelling

Our research focuses on the development, implementation, and application of novel statistical models for stochastic processes. A stochastic process is a random variable that is observed over time, for example, the maximum depth of a marine animal's dive (observed over multiple dives), daily returns of a company's stock (observed over multiple days), or the number of goals scored per match by a football team (observed over multiple matches).

Method development

We develop and implement novel statistical models that help generating knowledge from data. In particular, we are interested in hidden Markov models (HMMs), Markov-switching regression models, and stochastic differential equations (SDEs). These are useful to investigate how the properties of a stochastic process change over time, and how these changes can be explained by covariates.

Applications in ecology

We apply novel statistical models to animal movement data collected by telemetry sensors such as GPS, dive, and acceleration data. Due to the ongoing big data revolution in ecology caused by technological advances in bio-logging technology, there is a high demand for special-purpose models that help exploiting the potential of such data. For example, we use HMMs and SDEs to investigate how narwhals outfitted with GPS and dive sensors react to changing environments, such as human-induced sounds caused by vessel traffic.

Applications in economics

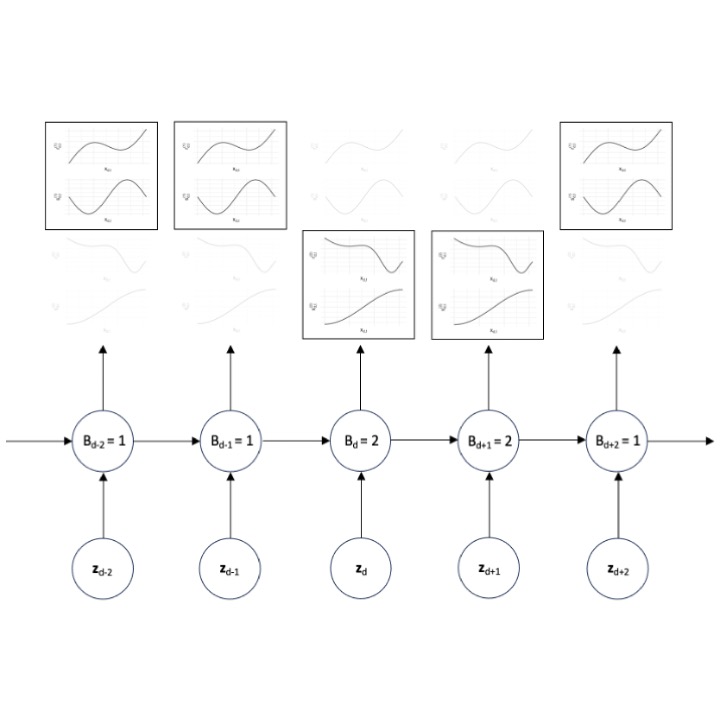

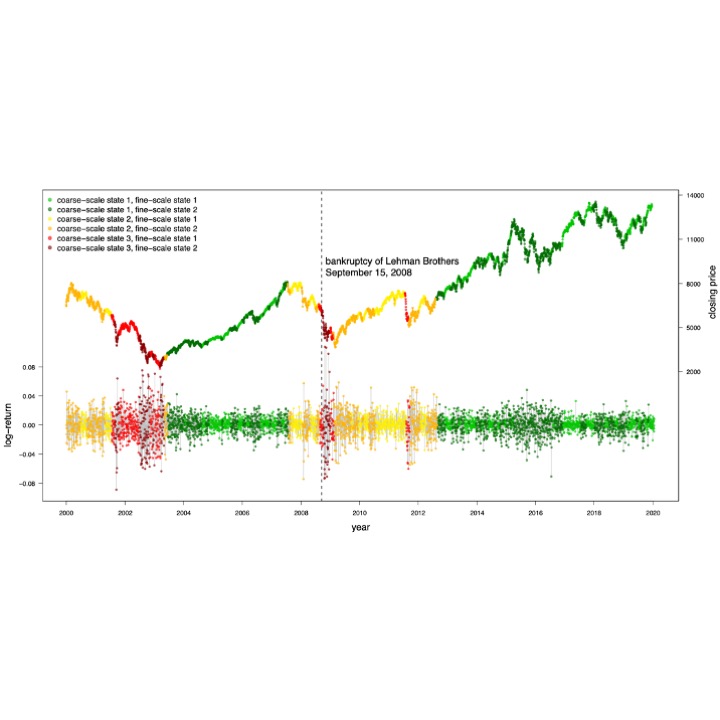

We apply novel statistical models to economic data such as stock returns, economic indices, and energy prices. For example, we use hierarchical HMMs to detect bearish and bullish markets in financial data. Financial markets exhibit alternating periods of rising and falling prices. Stock traders seeking to make profitable investment decisions have to account for those trends, where the goal is to accurately predict switches from bullish to bearish markets and vice versa.

A list of publications can be found here (see also Timo's Google Scholar profile).